Auditing and Attestation- Certified Public Accountant (CPA) Practice Exam -

$69.00

- Buy to unlock unlimited access to all Quiz questions and Answers in this Quiz.

- After purchase you can print a PDF of the whole quiz at any point. The PDF will contain the questions and the correct answers.

About this Exam

The Certified Public Accountant (CPA) license is the gold standard of qualification in the accounting profession, signifying a high level of technical skill, ethical commitment, and professional dedication. To earn this prestigious designation, candidates must pass the rigorous Uniform CPA Examination, which consists of three Core sections and one Discipline section.

The Auditing and Attestation (AUD) section is one of the three mandatory Core components. It is specifically designed to assess a candidate’s knowledge and skills related to the entire auditing process for various entities, including public and private companies, governmental entities, and not-for-profit organizations. This exam is essential for aspiring auditors, assurance professionals, and accounting students who intend to perform attestation engagements, express opinions on financial statements, or specialize in internal controls and compliance. Passing AUD demonstrates that you possess the critical thinking and conceptual understanding required to safeguard the integrity of financial reporting.

Ready to test your knowledge?

Buy Now to Access

Additional Information

What the Course Entails and Exam Details

Preparing for the AUD section requires a deep understanding of the standards and procedures governing auditing and other attestation engagements. The content is heavily based on the AICPA CPA Exam Blueprints, which organize the necessary knowledge into four primary content areas, each weighted differently:

Area I: Ethics, Professional Responsibilities, and General Principles (15–25%): This section covers the foundational aspects of the profession, including requirements for independence, professional skepticism, professional judgment, and ethical conduct under the AICPA Code of Professional Conduct, as well as standards set by the PCAOB, SEC, GAO, and DOL.

Area II: Assessing Risk and Developing a Planned Response (25–35%): Candidates must master engagement planning, understanding the entity and its environment (including internal controls, COSO framework, and IT systems), materiality, and assessing the risks of material misstatement, whether due to fraud or error.

Area III: Performing Further Procedures and Obtaining Evidence (30–40%): This is the largest section, testing the actual execution of an audit. It covers sufficient appropriate evidence, sampling techniques, specific audit procedures (test of controls, analytical procedures, external confirmations), and special considerations such as accounting estimates and subsequent events.

Area IV: Forming Conclusions and Reporting (10–20%): The final area tests the ability to evaluate misstatements, form an appropriate audit opinion (unmodified, qualified, adverse, disclaimer), and prepare different types of reports for audit, review, and compilation engagements (SSARS and SSAE standards).

Unlike some accounting exams that rely heavily on calculations, AUD is highly conceptual. It demands that you not only memorize terms but also understand the context and purpose of auditing standards to apply them to real-world scenarios.

What to Expect in the Final Exam

The actual AUD section of the CPA Exam is a comprehensive, four-hour assessment. You must understand the structure and time constraints to succeed.

Exam Format: The exam consists of 72 Multiple-Choice Questions (MCQs) and 8 Task-Based Simulations (TBSs).

Structure: The exam is administered in five separate testlets. The first two testlets contain the MCQs (36 per testlet). The last three testlets present the TBSs (2 in Testlet 3, 3 in Testlet 4, and 2 in Testlet 5).

Scoring Weight: Your score is determined by a 50/50 split between your performance on the MCQs and the TBSs. Both sections are equally important.

Time Limit: You have a total of 4 hours of testing time. A standard, 15-minute break is offered after the third testlet (after completing the first set of simulations), which does not count against your total 4-hour clock. You can take other breaks, but the clock will continue to run.

Passing Score: The CPA Exam is scored on a scale of 0 to 99. You must earn a minimum scaled score of 75 to pass the AUD section. This is a scaled score, not a simple percentage of correct answers.

How to Study and Exam Centers

Effective preparation for AUD goes beyond passive reading. You need an active study strategy focused on application and endurance.

Study Strategies:

Emphasize Concept Over Memorization: AUD is famous for subtle wording. Do not just memorize rules; understand the intuition behind why certain procedures are necessary and when they are required. Ask yourself: "How would this affect the auditor's opinion?"

Master Task-Based Simulations: TBSs are critical. Practice simulation types that require you to review exhibits (like emails or contracts), calculate materiality, or propose adjusting journal entries. Many candidates struggle with simulations because they do not practice them enough.

Use High-Quality Practice Exams: Integrate full, timed CPA AUD Practice Exams into your final weeks of review. This is essential for building testing stamina and mastering time management, ensuring you have enough time to complete the simulations in the later testlets.

Identify Your Weak Areas: Use the data from your practice quizzes to identify content areas (e.g., SSAE reports vs. SSARS compilations) where you are struggling. Dedicate extra study time to those specific AICPA Blueprint topics.

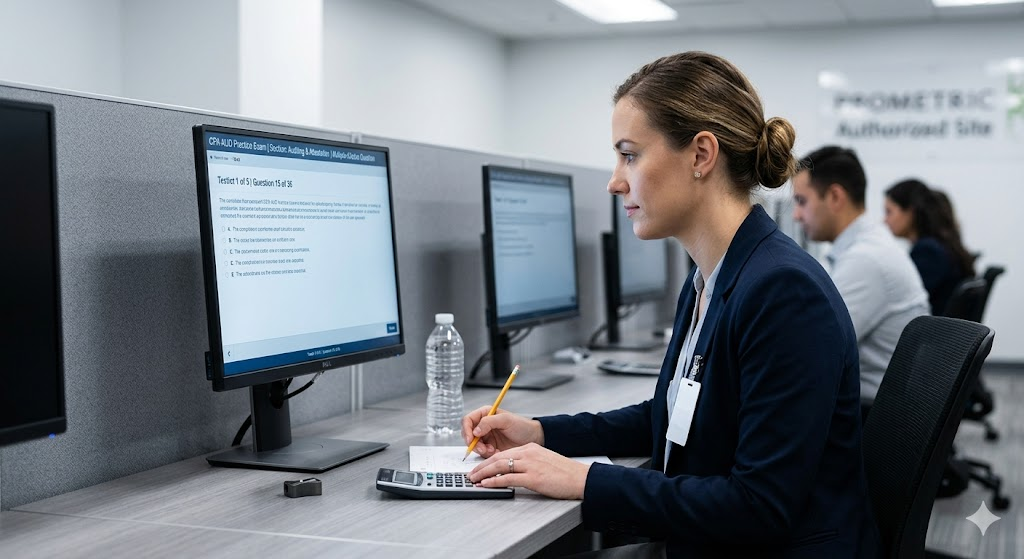

Exam Centers: The Uniform CPA Exam, including the AUD section, is not offered online or through authorized schools. It is administered exclusively in a secure proctored environment at Prometric testing centers located throughout the United States and internationally. To take the exam, you must first apply through your State Board of Accountancy and receive a Notice to Schedule (NTS) from NASBA. Once you have your NTS, you can visit the Prometric website to locate the nearest testing center and schedule your specific exam date within your eligibility window.

Job Opportunities from the Course

Passing the AUD section is a vital step toward obtaining your CPA license. Once licensed, an expertise in auditing and attestation, validated by this exam, opens the door to a diverse and rewarding range of career paths.

Some of the job opportunities unlocked by a CPA designation include:

Public Accounting (Big Four, National, and Local Firms):

External Auditor (Associate, Senior, Manager, Partner)

Assurance Associate

Risk Advisory and Compliance Manager

Internal Controls Auditor

Private Industry (Corporate Accounting):

Internal Auditor

Compliance Officer

Financial Controller

Chief Financial Officer (CFO) (often requires an auditing background)

Governmental Accounting and Non-Profit:

Government Accountability Office (GAO) Auditor

State Auditor / State Comptroller

IRS Criminal Investigation Agent

Specialized Roles:

Forensic Accountant / Fraud Examiner

Information Systems and Controls Auditor (integrating auditing with technology)

Each path offers a competitive salary, professional stability, and significant opportunities for advancement.

Frequently Asked Questions

Reviews

5.0

Based on 0 reviews

Leave a Review

No reviews yet. Be the first to review!